Jensen Huang didn’t go to Seoul to eat Korean barbecue. He went to lock in the most strategically important supply chain in AI hardware — and what happened over the past week reshapes how traders should think about the next leg of the semiconductor trade.

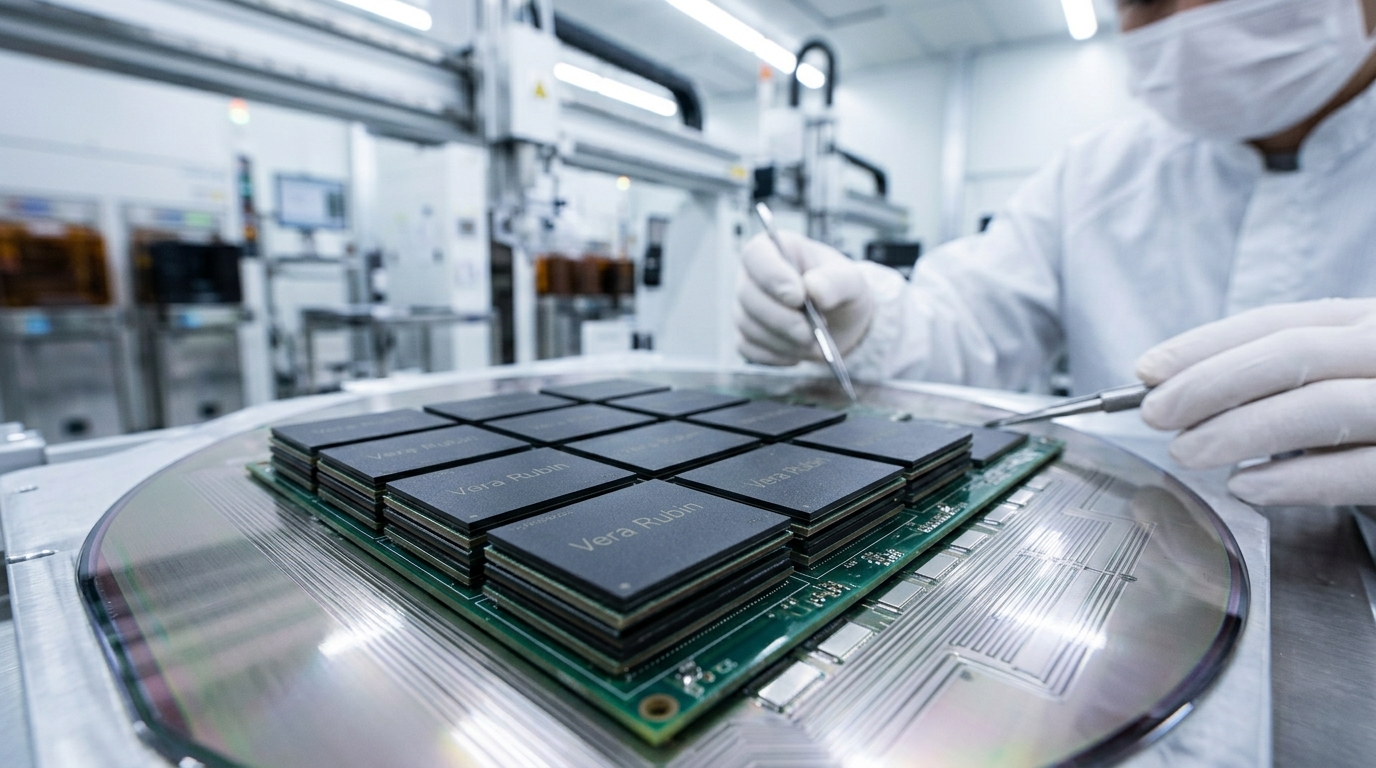

Here’s the headline: Nvidia’s Vera Rubin AI accelerator platform is now in full production. At the GTC Taipei keynote on June 1, Huang confirmed Samsung, SK Hynix, and Micron have all been certified to supply HBM4 high-bandwidth memory for Vera Rubin — ending months of supply-chain speculation. Deliveries to AWS, Google Cloud, Microsoft Azure, and Oracle are scheduled to begin Q3 2026.

Then Huang flew to Seoul. The meetings there weren’t ceremonial.

The Numbers That Define the Platform

Vera Rubin delivers 10x agent throughput compared to the Grace Blackwell architecture it replaces. Each server system pairs Vera CPUs with Rubin GPU clusters and terabytes of HBM4 memory. Supply-chain analysts estimate SK Hynix holds 60–70% of the HBM4 volume allocation, Samsung roughly 25–30%, and Micron the remainder. SK Hynix entered qualification ahead of both rivals. Samsung began HBM4 mass production in February 2026.

NVDA itself has a market cap of approximately $4.96 trillion as of June 8, with a 52-week range of $140.86–$236.54 and an all-time high of $236.54 set on May 14, 2026. The stock pulled back to the $204 area last week, pressured by the broader semiconductor selloff following Broadcom’s guidance — Micron fell 6.3%, Marvell lost 8%, AMD dropped 6.3% on June 5 alone. NVDA held its ground better than peers, gaining 1.82% on the day Huang announced the Vera Rubin supply certifications.

Slight tangent, but worth noting: Huang wrote “Please Make More” on an SK Hynix HBM4E wafer at the Computex booth and signed it. It was a gesture. It was also a very public signal of how tight the memory supply equation remains entering the second half of 2026.

Sector Breakdown — Where the Real Flow Is

The Vera Rubin announcement triggered a surge in Korean tech on June 1. Samsung Electronics closed up 10.1% at a record high. LG Electronics gained nearly 30%. Korean names moved because the supply-chain relationship just got formalized at scale — and the partnership scope expanded well beyond memory chips.

NVIDIA and LG Group announced plans to build an AI factory supporting LG’s robotics, autonomous driving, and data center technologies. SK Telecom plans to build a gigawatt-scale AI cloud in South Korea using the NVIDIA DSX platform, with the first AI factory expected online in 2027. Naver will scale sovereign AI infrastructure to 55 megawatts initially, with plans toward gigawatt capacity. Doosan Electronic Materials is expected to exclusively supply CCL materials for Rubin chips, with projected sales reaching KRW 1 trillion by 2026.

This is capital rotation — not just from chips to memory, but from pure GPU plays into the physical AI infrastructure buildout. Robotics, power, data center materials, sovereign cloud. The playbook is expanding.

What the Vera Rubin Ramp Implies for Positioning

- HBM4 demand is structurally undersupplied. Huang publicly urged SK Hynix to ramp faster on June 2, telling reporters that global semiconductor supply remains tight. When the CEO of the world’s largest company by market cap says that publicly, it’s not spin — it’s a procurement signal.

- The supply-chain assembly time improvement is significant. Huang noted rack assembly time for Vera Rubin has fallen from roughly two hours per rack to five minutes. That’s a manufacturing velocity story, not just a product story.

- The follow-on platform is already scheduled. Vera Rubin Ultra, using next-generation HBM4E memory, is expected in late 2027. That means the memory demand cycle extends well beyond the current quarter.

Technical Framework

NVDA’s recent range: $204 support zone on the low end, $218–$220 as the near-term resistance cluster where the stock was trading earlier this week before the broader tech tape softened. The 52-week high at $236.54 remains the structural target for bulls. Volume on June 5 ran at 219.66 million shares against a daily average of 191.33 million — elevated, consistent with institutional repositioning rather than retail momentum chasing.

The broader semiconductor index found its footing after a rough week. What matters going forward is whether Vera Rubin shipments in Q3 produce revenue confirmation. Nvidia’s next earnings are scheduled for August 26, 2026.

Scenario Modeling

Bull Case: Vera Rubin ships on schedule in Q3, early cloud provider deployments report throughput data validating the 10x performance claim, SK Telecom’s gigawatt AI factory accelerates. NVDA reclaims $220+, memory suppliers see sustained margin expansion. The Korean AI ecosystem trades as a secondary derivative play.

Base Case: Vera Rubin ramps smoothly but HBM4 supply constraints create modest shipment friction through Q3. NVDA consolidates in the $200–$220 range, with a catalyst setup into August earnings. Memory suppliers trade with high correlation to each Huang public statement.

Bear Case: Broader tech selloff deepens, the jobs data / rate narrative pressures risk assets, and Vera Rubin faces qualification delays at the hyperscaler level. NVDA tests the $190–$195 zone. Korean supply-chain names give back the June surge.

Active Trader Framework

The $204 level on NVDA is the line to watch on the downside — that’s where the recent range low printed. A clean hold and volume expansion above $218 reopens the path toward $236. For traders focused on the supply chain angle rather than NVDA directly, SK Hynix and Micron (MU) offer differentiated exposure with distinct risk profiles — SK Hynix holding the dominant volume share but trading on Korean exchange, Micron the most accessible domestic proxy despite its smaller Vera Rubin allocation.

Risk management consideration: this is a catalyst-driven trade with a known binary event in August earnings. Position sizing relative to that volatility window matters more than entry precision right now.

The macro context reinforces the setup. AI infrastructure spending across the four mega-cap hyperscalers is tracking toward roughly $710 billion in 2026 combined capex. That capital has to go somewhere in the supply chain — and Huang just told you exactly where.

For informational and educational purposes only. Not investment advice. Trading involves risk, including loss of principal.